The U.S. housing market is showing new signs of strain. According to recent data from the Mortgage Bankers Association, in the third quarter of 2025, the total mortgage delinquency rate remained flat at 3.93%. While overall delinquencies remained flat compared to last year, the composition shifted, with early-stage delinquencies declining and serious delinquencies rising, inching closer to the foreclosure status, which may be a precursor to a housing bubble. The rate for conventional loans declined slightly, but FHA and VA loan rates increased.

This shift may be one of the first signs that many homeowners are struggling to keep up with higher mortgage payments, inflation, and debt, which was a recipe for disaster in the 2008 housing crisis. As consumers deal with this increasing pressure, financial and credit education are more important than ever.

“The increase in mortgage delinquencies is a clear sign that household budgets are being stretched thin,” said Robin Clayton, Vice President of Consumer Finance and Education at CreditBuilderIQ. “Even a single missed payment can have lasting effects on a consumer’s credit profile. Now is the time for homeowners to review their budgets, explore refinancing or assistance options, and stay proactive in managing their credit health.”

CreditBuilderIQ is a DIY credit-building innovative tool offered by the financial intelligence company IDIQ that allows consumers to better understand, track, and improve their credit and financial health. Through educational insights, credit monitoring, and actionable tools, CreditBuilderIQ helps homeowners strengthen their financial habits and make informed decisions before a missed payment negatively impacts financial goals.

Rising Delinquencies: What It Means for Homeowners

Rising delinquency rates serve as an early warning sign for broader financial stress. When a homeowner becomes seriously delinquent, which is typically defined as 90+ days past due, it not only impacts the property and loan but also the individual’s credit file. Lenders may view increased delinquency trends as a signal that income, savings, and finances are no longer stable.

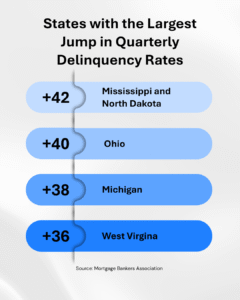

Regional Hotspots Reflect National Trends

Looking beyond the national average, there are regional spikes in delinquency rates with areas of concentrated risk. At highest risk are Mississippi and North Dakota, both registering +42 basis points in quarterly increases.

Ohio, with +40 basis points, and Michigan, with +38, suggest the Rust Belt and industrial states continue to feel pressure from shifting job markets and stagnant wage growth.

West Virginia follows with +36 basis points to flag a region where income levels and economic mobility have long been challenged.

Why Credit Education Matters More Than Ever

Financial literacy is essential to understanding your options when facing mortgage pressures. Homeowners must understand how mortgage terms, credit scores, payment history, and payment delinquencies affect their credit scores. Education allows borrowers to take corrective action, which can mean refinancing, seeking loan modification, or reducing other debt. Tools and platforms that build credit are essential to this process.

How CreditBuilderIQ Can Help Homeowners

CreditBuilderIQ helps homeowners take control of their financial health through clear, easy-to-understand credit education and actionable steps to strengthen their finances and credit profiles. The platform breaks down how factors like payment history, credit utilization, and delinquencies affect your credit score, so homeowners can make informed decisions before small issues become major setbacks.

With personalized insights and tools, homeowners can learn how to rebuild their credit, conquer their debt, and improve borrowing potential to protect their financial future.

Next Steps: What Homeowners Should Do Now

If you’re a homeowner concerned about delinquency risks, here are steps to consider:

- Review your mortgage terms and payment schedule. If you have an adjustable‐rate mortgage, explore whether refinancing into a fixed rate makes sense.

- Check your monthly budget and debt obligations. Are you setting aside funds for unexpected expenses or a disruption in your income?

- Review your credit score, credit history, and alerts. A missed payment or negative impact on your credit report can signal trouble ahead.

- Consider working with a credit-building service, such as CreditBuilderIQ. These services guide you through steps to protect your credit and finances, especially if your mortgage or other debt is under strain.

Bottomline

As mortgage delinquency rates rise across multiple loan types and regions, it’s clear that many homeowners are experiencing financial instability. With seriously delinquent rates up by tens of basis points in key states and across loan options, credit health and financial education have taken on an even more important role.

Homeowners can take control with credit-building and education services such as CreditBuilderIQ. Learn more about CreditBuilderIQ and how it can help you today.

")